Introduction

Investing is a critical component of personal finance, but the strategy that works best can vary significantly based on one’s stage in life. From young adults fresh out of college to retirees, understanding the most appropriate investment strategies for different life stages can enhance financial stability and long-term wealth accumulation. This article explores investment strategies tailored to various life phases.

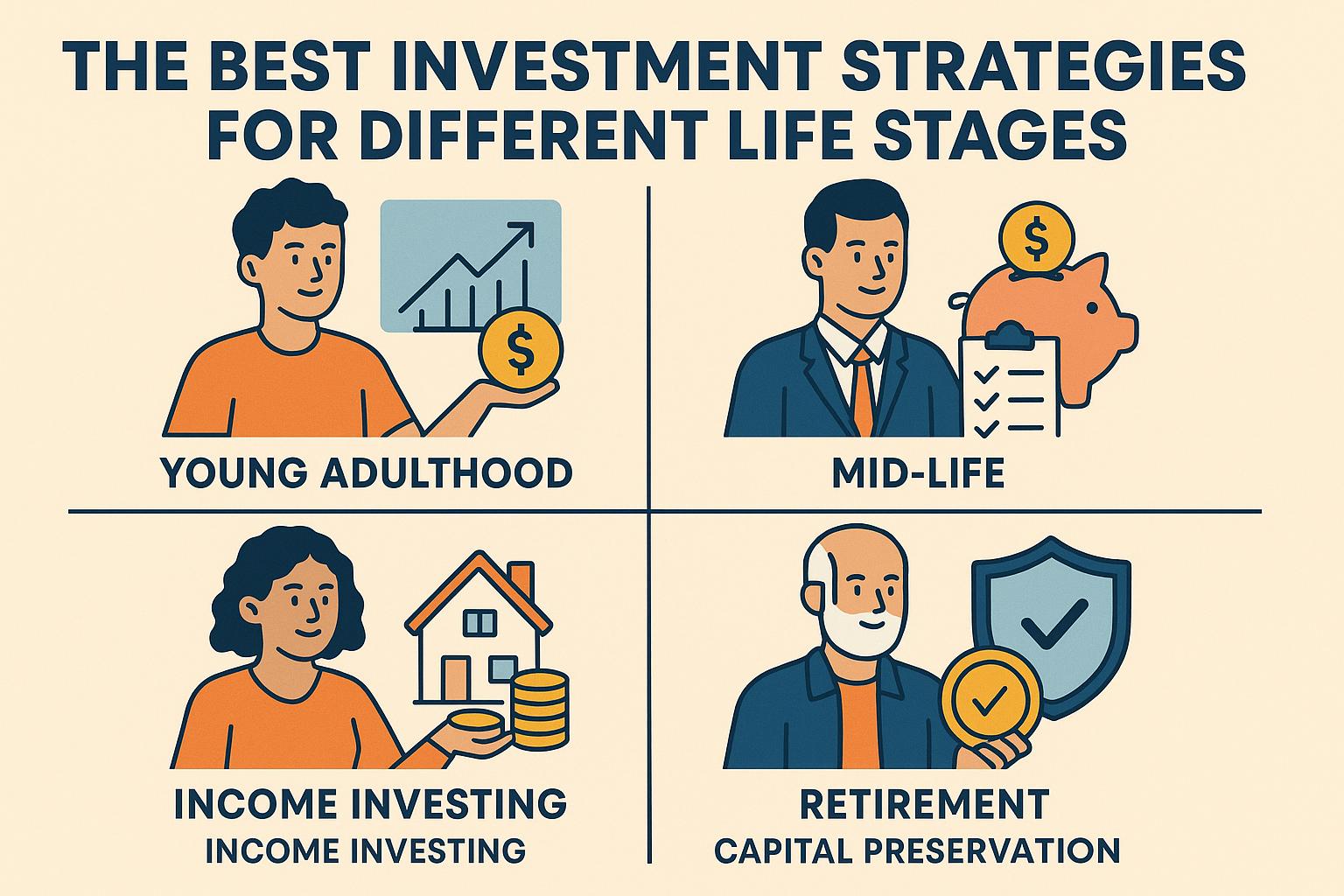

Early Career (20s to 30s)

In the early career stage, individuals often have limited financial obligations and a long-time horizon. This stage provides the opportunity to adopt a more aggressive investment approach. Young investors typically have the advantage of time, which allows them to recover from market downturns. Therefore, risk-taking with investments is often encouraged. Moreover, young adults are generally in a phase of their lives where capturing the upside potential of investments is vital for building long-term wealth.

Emphasizing growth, young investors can allocate a larger portion of their portfolio to stocks, particularly in high-growth sectors like technology and biotechnology. Though stocks are volatile, their historical performance suggests a potential for greater returns over time compared to more conservative investments.

Additionally, it’s paramount to start an emergency fund during these years. This fund serves as a safety net for unexpected expenses, helping to avoid withdrawing from investment accounts in emergencies, which could undermine long-term financial goals. An emergency fund should ideally cover three to six months of living expenses.

Young professionals should also utilize employer-sponsored retirement plans such as a 401(k). These plans not only offer tax advantages but also frequently come with employer-matching contributions, which is essentially free money. This can significantly boost a retirement nest egg through the power of compounding over the decades.

Mid-Career (30s to 50s)

During the mid-career phase, the financial landscape can become more complex, often involving higher income levels paired with increased expenses from supporting a family or paying a mortgage. It’s a pivotal time to ensure that investment strategies reflect both growth aspirations and risk management.

Diversification is crucial; it involves spreading investments across different asset classes to reduce risk. Including a healthy mix of bonds or indexed funds can provide a stable counterbalance to the potential volatility of stocks, thus aligning investments with a more balanced risk appetite.

Another pivotal component of a mid-career portfolio includes investing in real estate. Real estate can serve dual purposes: providing a personal residence and acting as a source of passive income and capital appreciation. Real estate often offers diversification beyond equities and can come with significant tax advantages, such as deductions on mortgage interest.

Moreover, with rising incomes, it’s wise to increase retirement contributions. Maximizing contributions to retirement accounts not only prepares for the future but also exploits available tax savings and compound growth opportunities. It’s advisable to periodically review these contributions, ensuring they align with long-term objectives.

Late Career (50s to 60s)

As individuals approach retirement, investment strategies often shift focus from aggressive growth to capital preservation. This transition aims to ensure that resources will be sufficient to cover living expenses through retirement.

It becomes imperative to reduce portfolio risk. This usually means reallocating investments away from high-risk assets such as equities to more stable securities like bonds and fixed-income assets. The goal is to protect accumulated wealth from significant market downturns that might occur just as your earnings phase concludes.

Assessing retirement needs is often necessary as this stage involves estimating the future financial requirements to sustain a comfortable lifestyle post-retirement. Consulting with financial professionals can be beneficial in refining retirement strategies, defining income needs, and ensuring that investment portfolios match risk tolerance as retirement approaches.

Considering health care costs is also crucial because these expenses can increase significantly with age. Health Savings Accounts (HSAs) provide a mechanism to save for these costs with tax benefits, offering another means of preparing for post-retirement health care needs.

Retirement

Upon reaching retirement, the investment strategy focus transitions to income generation and capital preservation. The primary concern often involves maintaining the lifestyle established during working years without the financial fallback of active income.

To create an income stream, some retirees invest in annuities, stocks with dividends, or construct bond ladders. These types of investments can provide a steady cash flow, which is essential for daily living expenses.

Managing withdrawals carefully is necessary to ensure that savings last throughout retirement. The frequently cited 4% rule can serve as a guide for sustainable withdrawals, suggesting that withdrawing 4% annually from the retirement savings is likely to provide adequate income while maintaining the savings’ longevity.

Lastly, it’s essential to stay informed and continue reviewing and adjusting the investment strategy to reflect changes in both personal financial circumstances and the broader market environment. Regular portfolio reviews can keep retirees abreast of necessary changes, ensuring ongoing financial stability.

Conclusion

Investment strategies should adapt at each life stage to optimize financial growth while mitigating risks. By understanding the distinct challenges and opportunities at different phases of life, individuals can craft a suitable investment approach. For further reading on financial planning and investment strategies, consider exploring industry blogs and financial resources that provide expert analysis and guidance.

This article was last updated on: November 21, 2025